TPG’s $7.6B Acquisition of AT&T’s DirecTV Creates Cable Giant

Isabel O'BrienYou’re reading Value Add’s weekly briefing, the leading newsletter for the operating side of private equity. Here’s what you need to know this week, from insights for PE-backed executives and portco news to recent buyouts and investment trends.

Insights

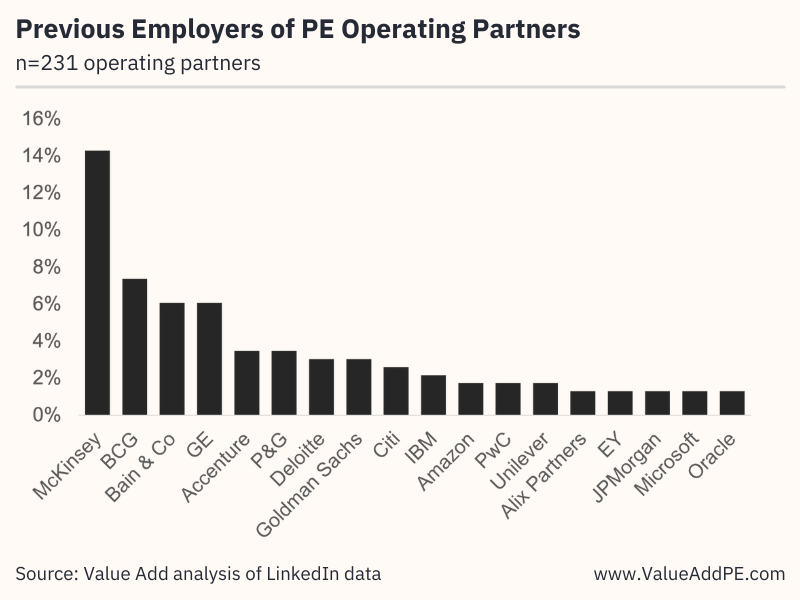

Chart of the Week: Outside of consulting, the most common pathway to a private equity operating partner role is through corporates that have well-established leadership development programs, according to research from Value Add. However, as the data shows, representation from corporates is quite fragmented among operating partners. This makes sense given that different PE firms value different types of industry experience depending on their own investment theses. (Read More)

More Insights

- Are PE-Backed Companies More Likely To Go Bankrupt? It’s Complicated. (Read)

- Apollo: “You Can’t Talk in the ESG, Alphabet-Soup Jargon” to CFOs (Read)

- Exits Are More Sensitive to Interest Rates Than Buyouts (Read)

- History Shows Interest Rates Alone Have Marginal Impact on Buyout Activity (Read)

- “We’ve Moved Downmarket”: Behind Riverside’s Unique Roll-Up Strategy (Read)

Spotlight

I stream, you stream. TPG first bought a stake in DirecTV in 2021, when it bought a 30% stake in the business for $1.8 billion as parent company AT&T spun it out, giving the new business a $16 billion total valuation.

Now, three years later, TPG is taking the remaining 70% stake in the company – again, from AT&T, and for $7.6 billion. The deal is expected to close late next year. AT&T will receive a payment of $2 billion upfront from TPG, and then incur more payments through 2029 totaling $7.6 billion. Current CEO Bill Murrow is expected to maintain his leadership position at DirecTV.

The two transactions are a far cry from the $48.5 billion AT&T agreed to pay Comcast-Time Warner for the business in 2014, implying a total business valuation of $67 billion. That’s likely because AT&T’s ownership of the company was hampered by high debts and dwindling cable subscriptions due to the rise of streaming services.

Dish it out. Distribution payments to DirecTV were down year-over-year in 2023, at $2.04 billion (compared to 2022’s $2.65 billion). Lucky for TPG, though, 2024 is due to be a better year, with projected distributions totaling $3 billion.

And that’s due to grow with DirecTV’s acquisition of competitor Dish, a cornerstone in TPG’s value creation plan.

DirecTV announced at the end of September that it was going to acquire its competitor, Dish, from Echostar, a satellite communications company. The price tag might seem low – just $1 – but it comes with the stipulation that DirecTV will assume Dish’s $9.75 billion in debt. As such, TPG and DirecTV are giving Dish a $2.5 billion loan to pay off its debt maturity by the end of November.

The deal will nearly double DirecTV’s current 11 million subscribers to 20 million – just shy of the all-time-high of 20.3 million subscribers that DirecTV had in 2015 when AT&T bought it. It will make the combined company the US’s largest pay-TV provider.

Subscriber growth is key to this merger: “We believe a combined DirecTV and Dish will be better positioned to work with programmers to allow us to deliver smaller, more flexible packages at lower price points, providing more choices and better value to consumers,” DirecTV’s chief advertising and sales officer, Amy Leifer, said in a LinkedIn post.

The two companies attempted to merge in a $19 billion deal in 2002, but it was struck down by antitrust regulators. Now that we have streaming and other mechanisms for watching content, it is likely that the deal can finally go through.

TPG did not respond to request for comment.

Buyout News

It’s been a busy week for TPG. Alongside its AT&T deal, it is also battling EQT and DigitalBridge (via their joint portfolio company Zayo Group) for Crown Castle’s fiber and wireless assets. The carve-out could be valued between $8 billion and $10 billion. It is possible that Crown Castle will sell just its fiber or just its wireless assets, with both subsidiaries being valued at less than $5 billion, or decide not to sell at all.

TPG is also looking to take a majority stake in Surescripts, a digital prescription service currently owned by CVS, Cigna subsidiary Express Scripts, and two pharmacist trade groups, all of whom will stay on as minority shareholders. The deal values the company at over $1.5 billion.

And finally, TPG is partnering with Singaporean sovereign wealth fund GIC to purchase Techem, a digital solutions provider for the construction industry, for €6.7 billion ($7.35 billion). The sellers are current majority shareholder Partners Group alongside minority shareholders CDPQ and OTPP. The deal will close in the first half of next year.

Also in the software space but not including the omnipresent TPG, Clearlake Capital and Francisco Partners have agreed to acquire Synopsys Software Integrity Group for $2.1 billion. The Massachusetts-based provider of application security services will be renamed to Black Duck Software.

Our last deal of the week comes out of left field when compared to the TPG- and software-centric deals above. Or comes out of… left winger?

Ares Management has become the first private equity group to throw its hat in the ring to buy a minority stake in an NFL team – the Miami Dolphins, to be exact. The NFL only recently allowed such transactions to take place this August. The deal, which would entail Ares buying a 10% stake in the team, its stadium, and the operating rights to the Miami Grand Prix and half of the Miami Open, implies an overall enterprise value of $8.1 billion.